The motor finance redress delay is not a reprieve

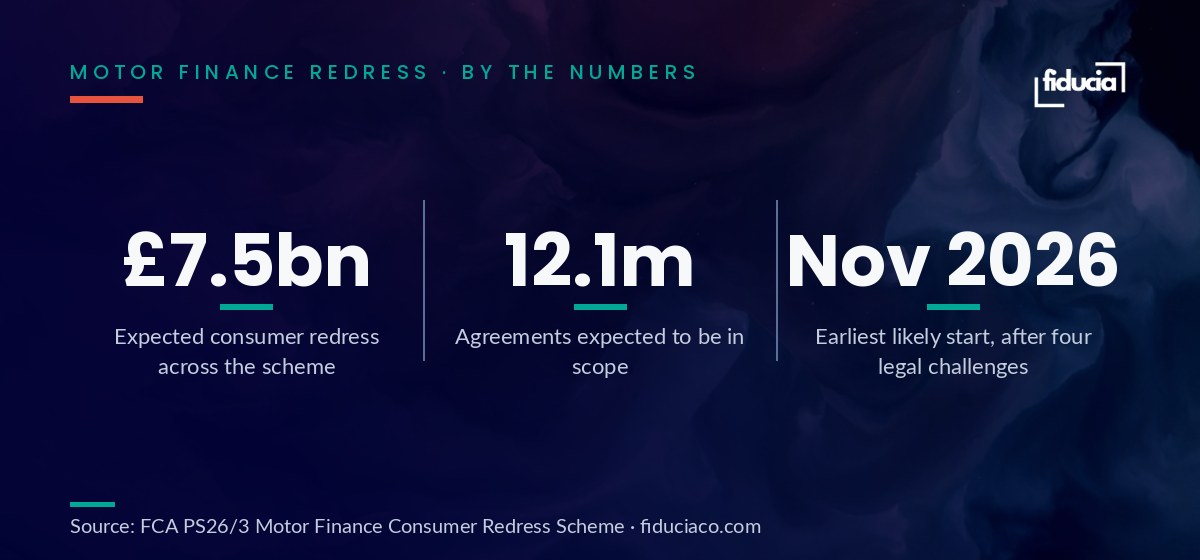

The number that should be on every motor finance board agenda this quarter is £7.5bn. That is the redress the FCA expects firms to pay across roughly 12.1 million agreements, at a total sector cost closer to £9.1bn once you add the cost of running it all.

Most firms braced for a 30 June implementation date. That date has now slipped. Four legal challenges, three from lenders and one from a consumer group, mean the scheme is unlikely to start before November 2026 at the earliest.

The easy read is that this buys time. It does not.

The delay changed the timing, not the work

The FCA has been clear on one point that is getting lost in the headlines. Firms are still expected to keep preparing while the courts do their work. That means identifying affected customers and collecting the historical data now, not after a ruling lands.

The scheme has two implementation tracks. Loans taken out from April 2014 sit under one deadline, older agreements under another. The court timeline pushes the start, but it does not pause the data archaeology, the case handling design, or the customer communications you will need to stand up at volume.

In our experience, the firms that treat a delay as breathing room are the ones that scramble later. The work does not get smaller because the date moved. It gets compressed into a shorter window when the ruling finally comes.

Why this is not a normal complaints exercise

Lenders run complaints functions every day, so there is a natural temptation to treat redress as the same job with a bigger queue. It is not.

A normal complaint arrives one at a time, and the customer brings the context with them. Redress runs the other way. You are proactively working out who is owed, reconstructing agreements you may not have touched in years, and applying a consistent calculation across a population measured in millions.

The volume is one problem. Consistency is the harder one. Two similar agreements that reach different outcomes because two assessors read the files differently is exactly the pattern a regulator looks for after the fact. At this scale, consistency cannot rely on individual judgement on every case. It has to be designed into the process.

What ready actually looks like

Readiness here is not a legal opinion. It is an operational capability, and it has three parts.

First, the data. Most lenders are sitting on agreements going back more than a decade, across systems that have been migrated, merged, or switched off. Finding every eligible agreement and reconstructing the commission position is a data engineering job, not a compliance memo.

Second, the case handling. When the scheme starts, you will be assessing cases at a scale your current complaints function was never sized for. This is where the economics bite. Rules based and agentic automation can take the cost per case well below a manual only model, because the repetitive assessment work does not need a human on every step. The humans handle the edge cases and the sign off.

Third, the audit trail. Every redress decision needs to be explainable to a regulator after the fact. Build the decision log in from the start. Retrofitting an audit trail onto a process that was rushed live is how firms turn one remediation into two.

What to do in the next eight weeks

You do not need the final scheme rules to start the work that matters. In our experience the highest-leverage moves before any ruling are the unglamorous ones.

Scope the data first. Find out, honestly, how far back your records actually go and where the gaps are. This is usually worse than people expect, and it is the long pole in the tent.

Size the volume. Estimate how many cases you are likely to handle and over what window. That single number drives every resourcing and automation decision that follows.

Design the decision record now. Agree what every assessment must capture to be defensible later, before you build anything to produce it.

Then run a small pilot. Take a sample of real cases through end to end. You will learn more from fifty actual cases than from another month of planning slides.

The cheapest build time you will get

Our view is straightforward. The lull between the policy statement and the court ruling is the cheapest preparation time a firm will get. Capacity is available, delivery partners are not yet swamped, and you can build and test calmly instead of under deadline pressure.

The firms that wait for certainty will pay for that certainty twice. Once in rushed delivery, and again in the operational risk of getting redress decisions wrong at scale under a live regulatory spotlight.

A delayed scheme is not a smaller scheme. £7.5bn does not move because a hearing slipped to the autumn.

Not sure where automation pays for itself in your back office before the scheme starts? Answer 8 questions and get a personalised Intelligent Automation Readiness Score: where your highest-value opportunities sit, which processes are genuinely ready now, and what your first move is worth.

Tell us what is not landing

Tell us what you are rolling out and where adoption, automation or AI is sticking. We will come back with a clear plan for the first steps, what success looks like, and what it costs. No fifty-slide pitch.

Book a call